Can Digital Tools Cut Long Wait Times as Banks Fail to Catch Up?

March 30, 2023

As 2022–2023 reports show that consumers wait for too long and expect much more from their providers, banks need to step up.

The growing frustration with the banking sector

With the pace of the world today, it is no surprise that 76% of people expect to be engaged immediately when contacting their bank. However, in 2022, 39% of American respondents who visited a bank in person reported waiting more than they anticipated. What is worse, even after the queue, customers spend even more time filling out application forms and going through validation/verification, especially when opening an account.

Even though banks are taking steps to implement transformation initiatives, long wait times also affect digital channels. According to a 2022 study by Verint, 49% of potential customers start opening a banking account on the bank’s website. However, by the end of the day, the percentage declines to 34% for those who succeeded in finalizing the process. Most of those who failed to complete the registration end up with in-person assistance. Furthermore, 49% of respondents stated that resolving an issue with online access to their account took longer than expected.

This is confirmed by a 2022 report from Signicat: 68% of European consumers have abandoned the online account creation process midway through. Out of those people, 21% have cited the length of the registration process as the main reason, with another 21% saying that they were asked for too much personal information. Overall, 92% of respondents were concerned about the amount of data they share with a bank.

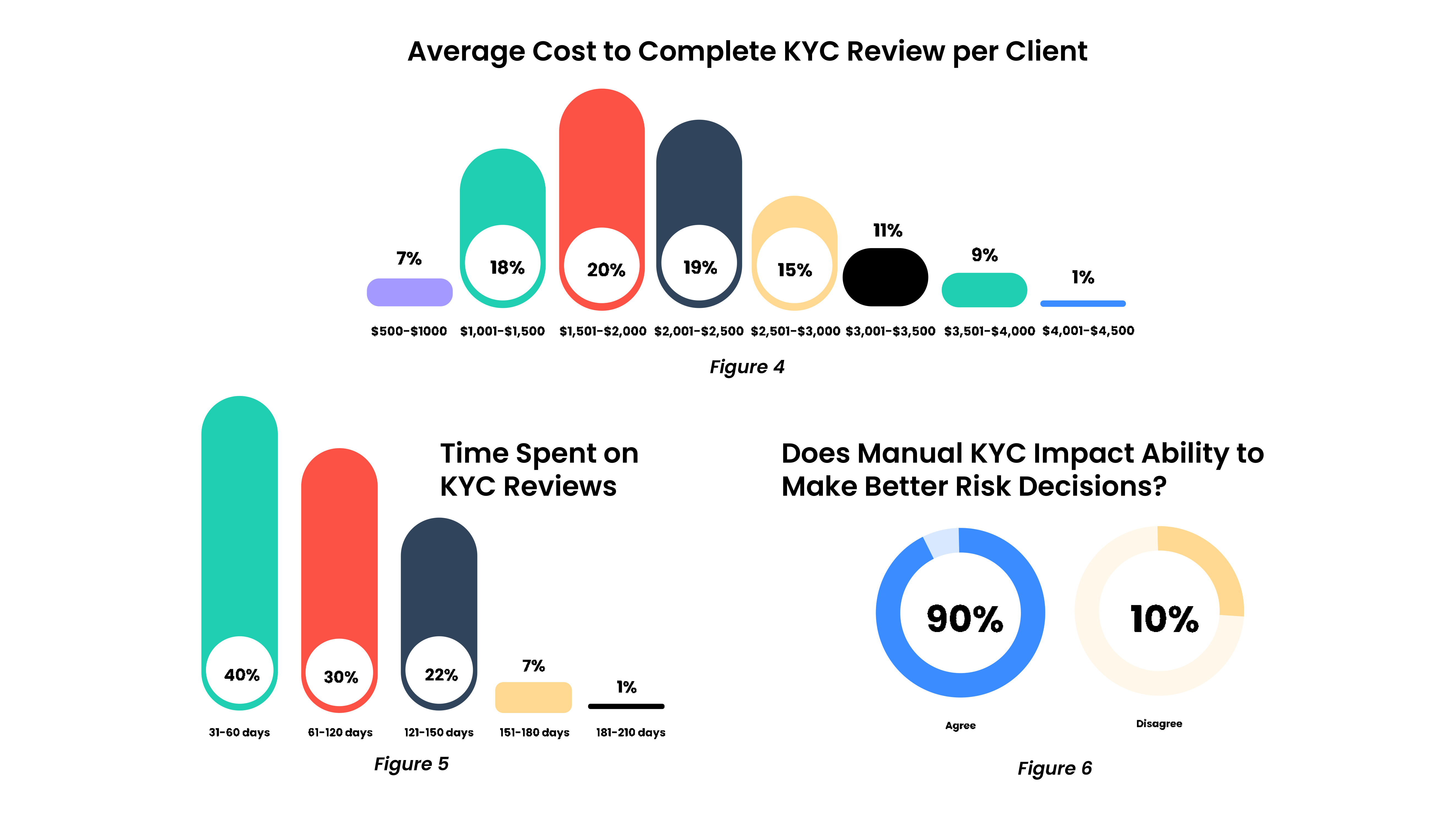

If manual customer verification procedures are involved, it can take weeks or even months before a person can actually use his/her account, a global 2022 report by Fenergo discovers. While the majority of requests are resolved within 1–2 months, in 22% of cases, the time spent on Know-Your-Customer (KYC) procedures may take 121–150 days.

Manual onboarding can take months (source: Fenergo)

Manual onboarding can take months (source: Fenergo)With the long wait times and convoluted processes, it is no wonder that bank customer satisfaction falls by 3% year-on-year, according to a 2022 study. 30% of Gen Z and Millenials admit that they would switch banks if it required no effort on their part.

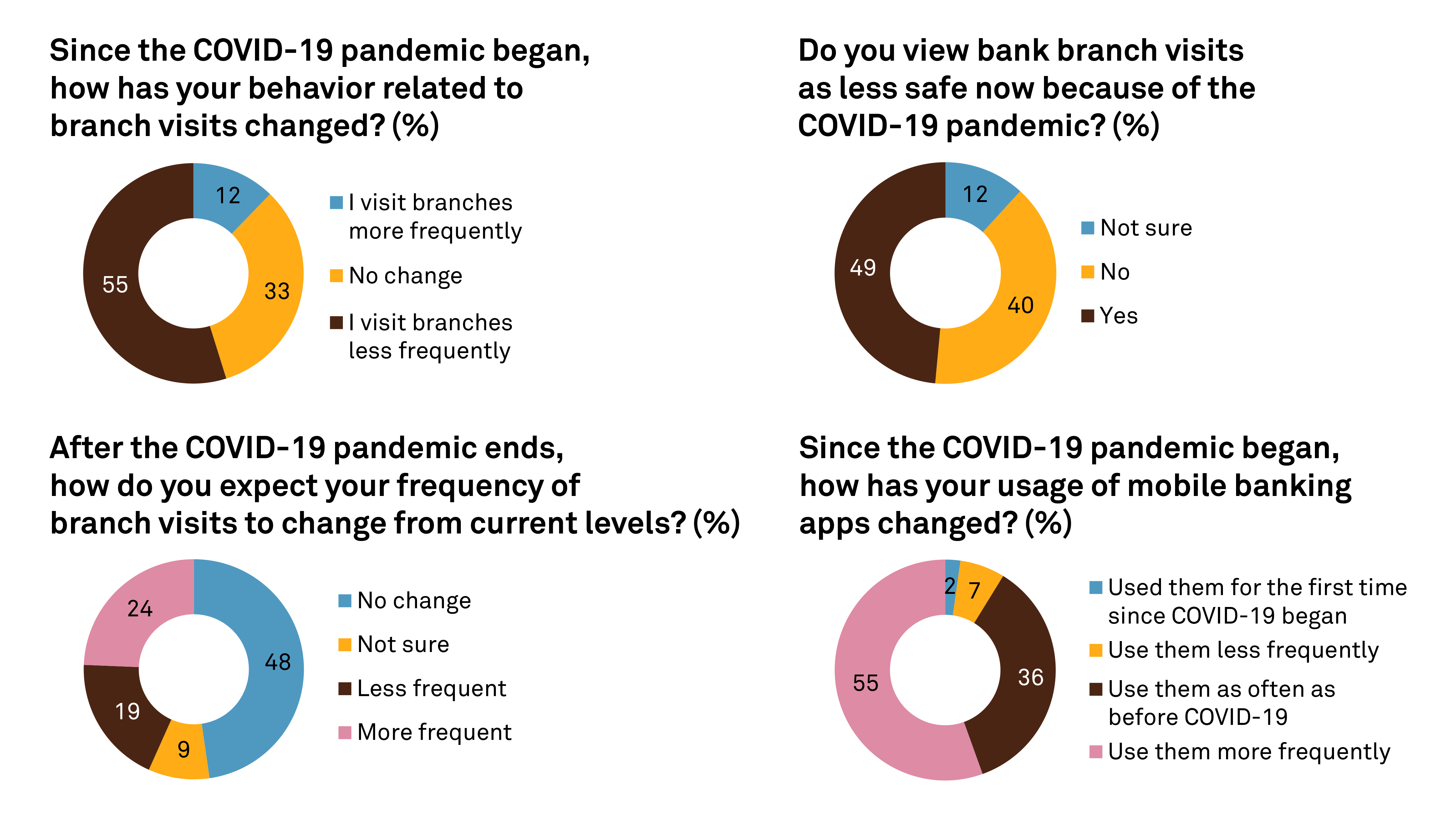

To stay competitive, traditional banks embrace digital transformation as a strategic priority, introducing online and mobile tools to enhance customer experience. The COVID-19 pandemic marked a turning point for online banking. According to S&P Global, US banks closed 2,927 branches in 2021 (over 2x more than in 2019). The use of digital tools for accessing personal finances has become a norm in Europe, too. For instance, a 2022 report from Ireland’s Department of Finance states that 63% of domestic customers are using online banking at least weekly.

The pandemic caused people to favor mobile banking (source: S&P Global)

The pandemic caused people to favor mobile banking (source: S&P Global)So, what do consumers value for digital banking today and what does it mean for financial institutions? Read on to learn.

Customers expect security and personal insights

While customers are forced to wait in queues and go through lengthy validation, their expectations stretch beyond faster service. Today, people want banks to be proactive in providing financial guidance, reminding about regular payments, and ensuring security, surveys say.

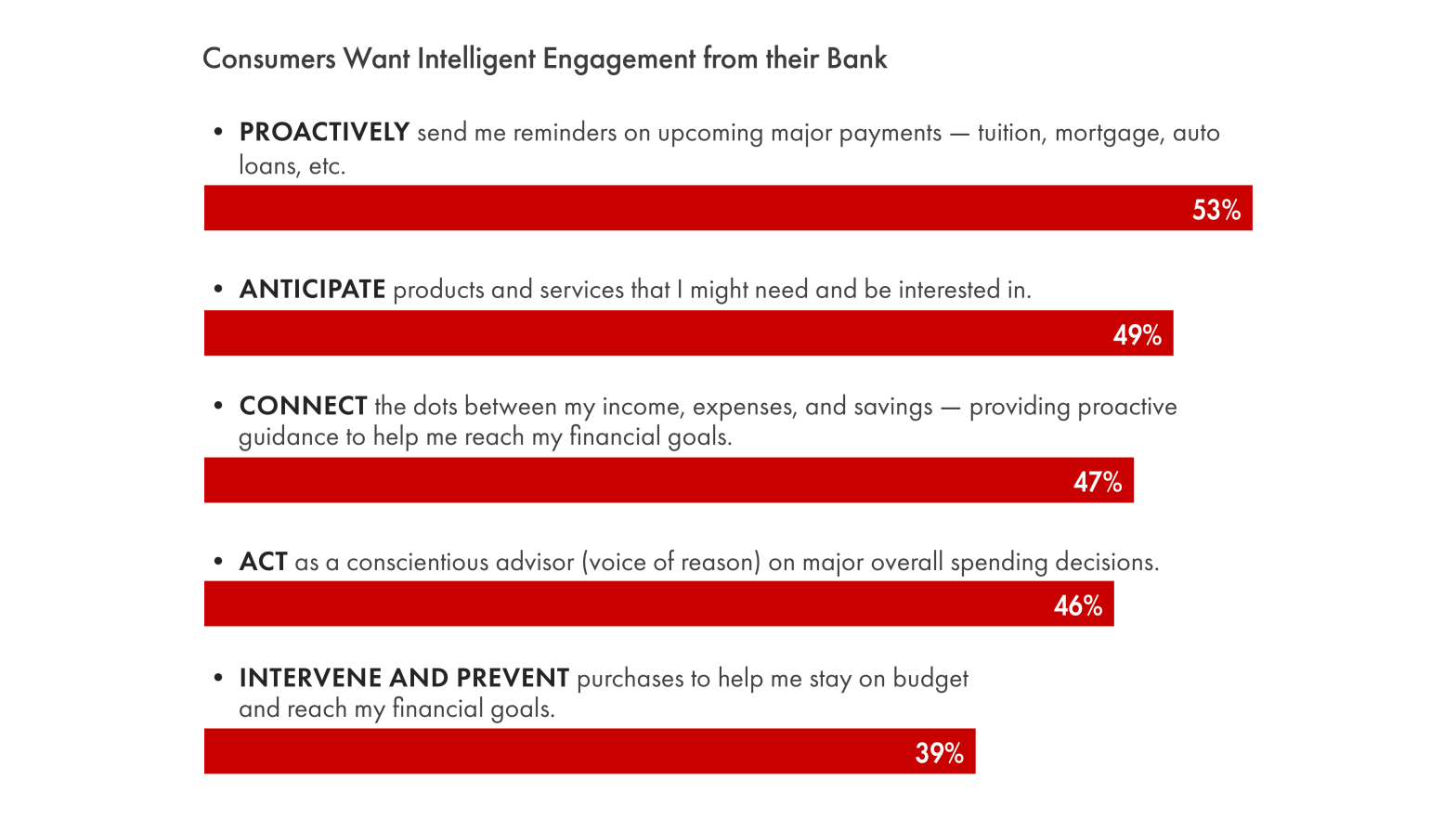

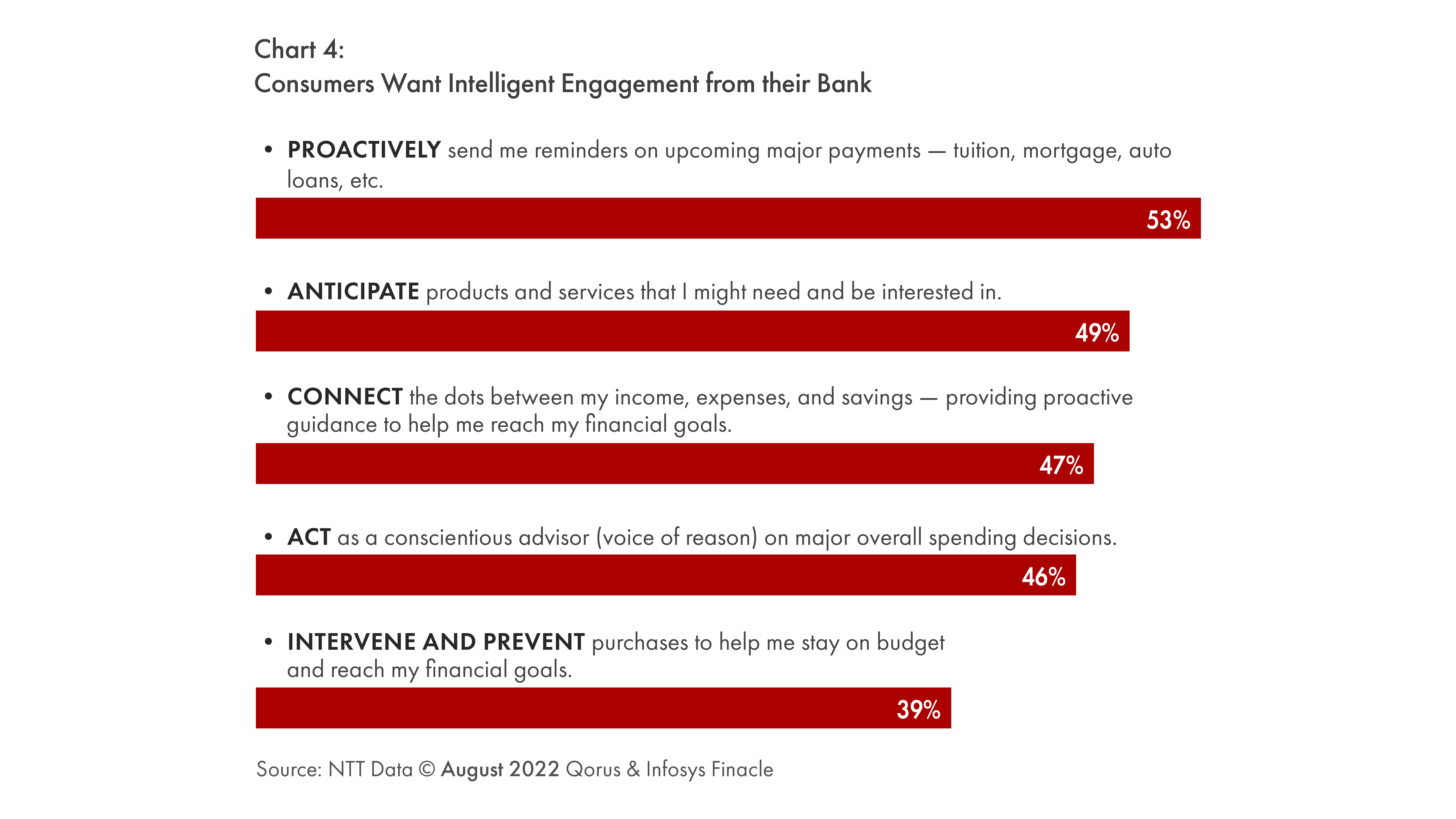

Specifically, an August 2022 report shows that 53% of users want to receive notifications about upcoming payments, such as tuition, mortgage, auto loans, etc. 47% of consumers want banks to analyze personal income, expenses, and savings information to help make better financial decisions. Notably, 46% of respondents want institutions to act as a trusted advisor for major spendings, and 39% would like their bank to help them stay on budget by preventing odd purchases.

Consumers expect more proactivity and personalization (source: Digital Banking Report)

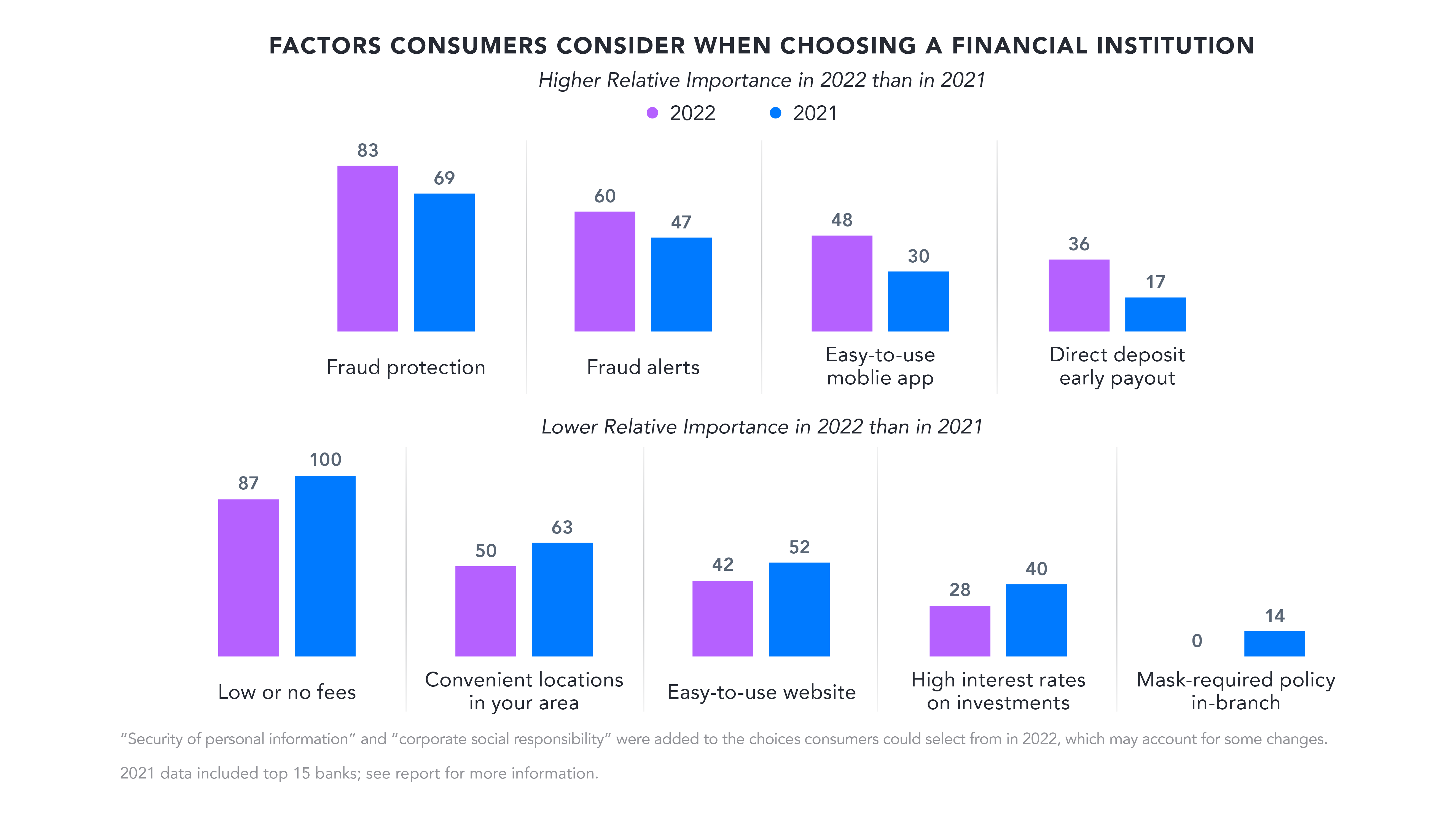

Consumers expect more proactivity and personalization (source: Digital Banking Report)As for security, the survey from Verint observed that fraud prevention was one of the most highly valued factors when picking an institution in 2022. Customers expect banks to monitor transactions for suspicious activity (e.g., someone trying to use your card in another country) and take preventive action.

56% of consumers consider Social Security number breach notifications extremely valuable, as indicated by a December 2022 report from Insider Intelligence. Unusual account activity notifications are appreciated by 51% of respondents. At the same time, 46% of people aged 41 and above are not aware that security notifications exist, while 22% don’t know how to turn on this functionality, Verint notes.

In general, the importance of digital channels for consumers is growing, while the location of physical branches becomes less relevant. Furthermore, compared to 2021, American users started to favor mobile apps over banking websites in 2022, the study from Verint says. In Ireland, for instance, the prevalence is even more significant: 69% prefer mobile apps to a bank’s website (22%), a government-issued survey detailed in 2022.

The growing importance of fraud protection and mobile apps (source: Verint)

The growing importance of fraud protection and mobile apps (source: Verint)The missing pieces

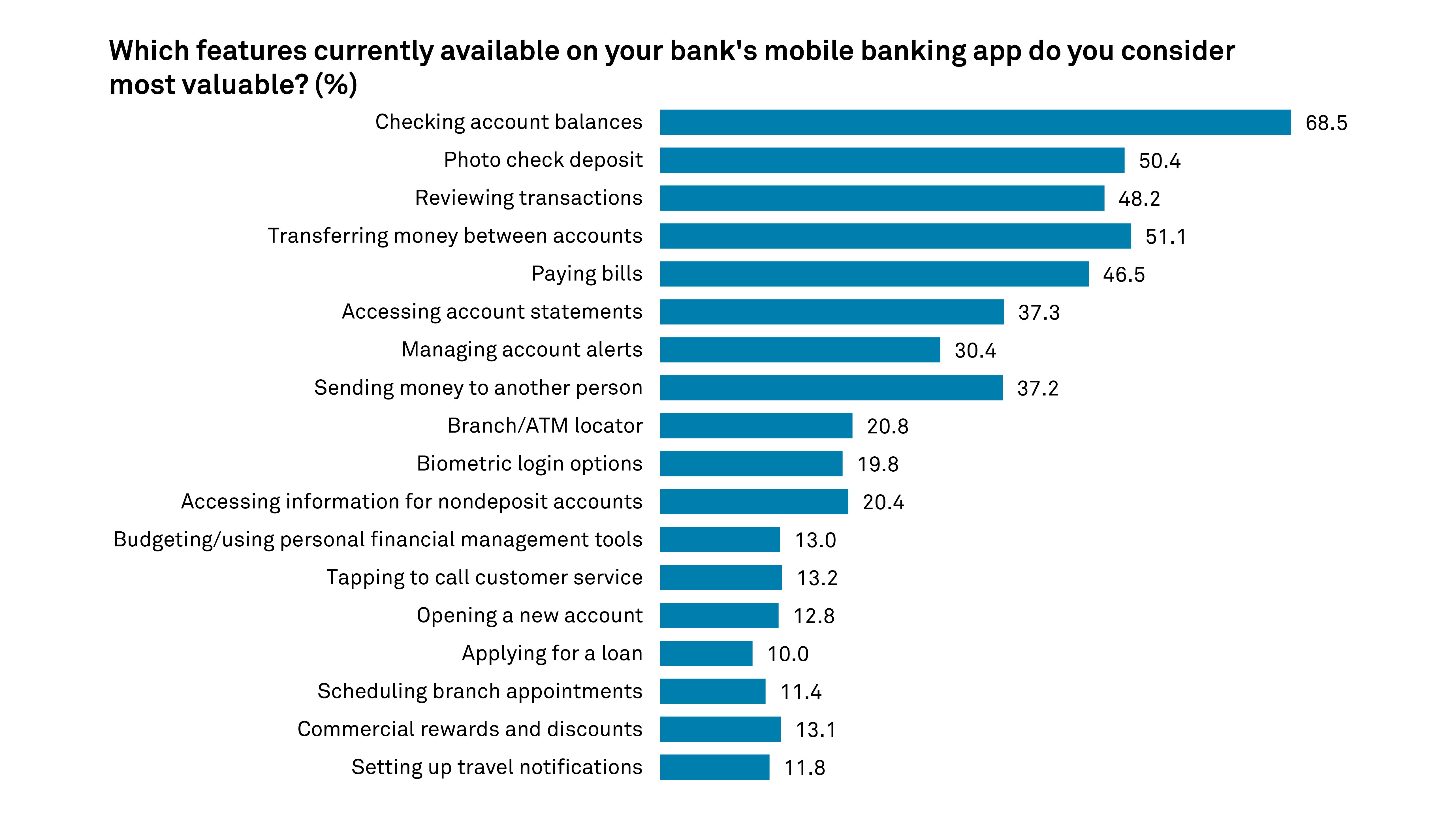

According to a 2021 report by S&P Global, the customers use mobile banking apps for the following most common scenarios:

- checking account balances

- transferring money between accounts

- depositing a physical check using the phone’s camera

- reviewing transaction history and accessing detailed statements

- paying bills and automating recurring transactions (for utilities, Internet, phone service, etc.)

People also often use banking apps to locate ATMs on a map, find a way to contact customer service, or schedule branch appointments in advance.

The most popular scenarios for using mobile apps (source: S&P Global)

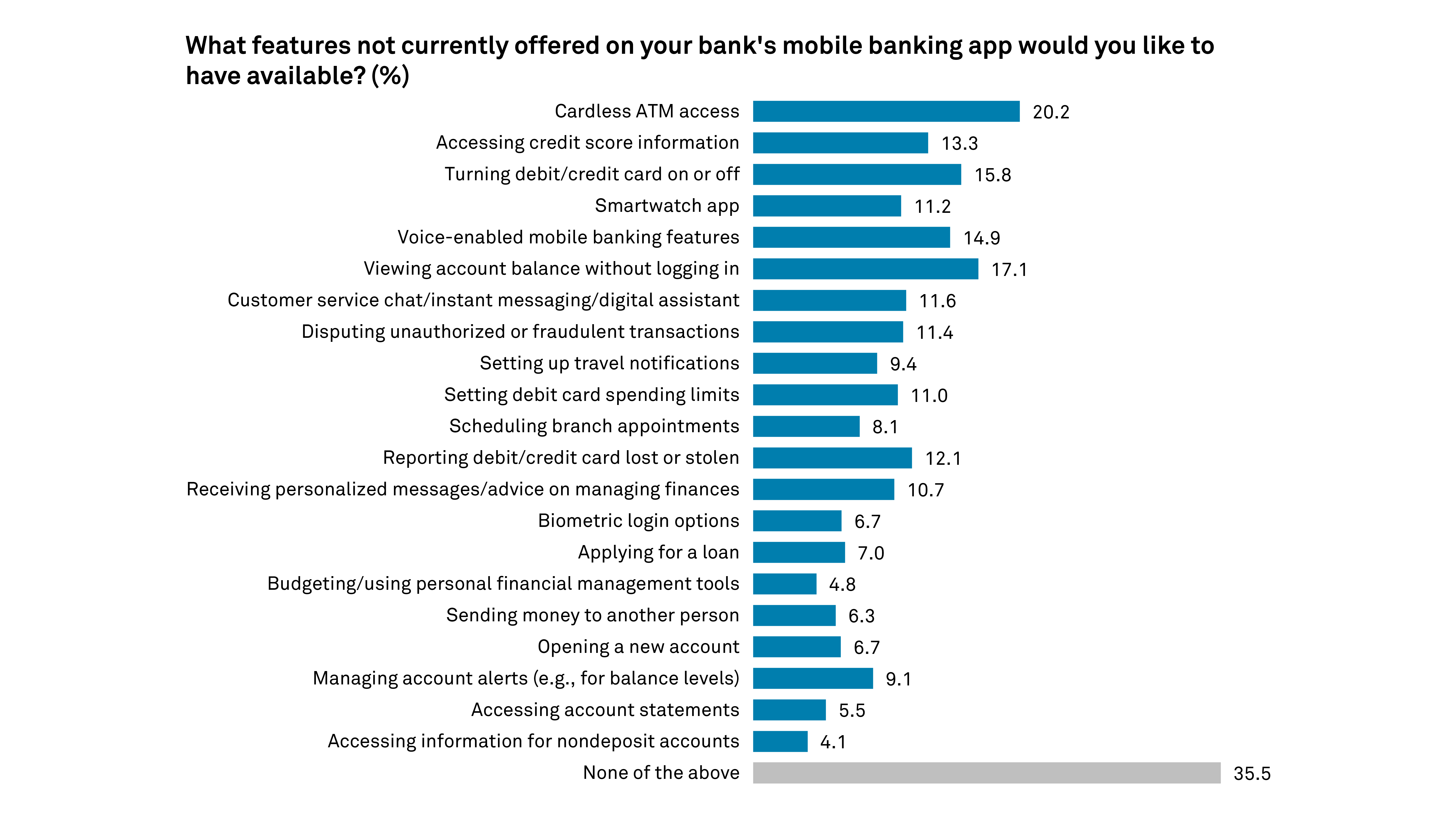

The most popular scenarios for using mobile apps (source: S&P Global)Despite the importance of mobile experience, there is a lot of highly requested functionality still not implemented in many banking apps. E.g., S&P Global’s report notes that customers from the middle Atlantic region of the US specify cardless ATM access as the most lacking feature.

Other welcome additions may include seeing the balance without logging in, (un-)blocking cards, as well as voice commands. The latter may range from asking Google, Siri, or Alexa for your balance to using voice for inputting transaction details or confirming payments within the app. Customers also want the ability to set spending limits, report a card lost/stolen, order a new one, view credit score details, dispute unauthorized/fraudulent transactions, chat, etc. Some of the users also would like to have a smartwatch version of the app.

Users expect much more than banks actually implement (source: S&P Global)

Users expect much more than banks actually implement (source: S&P Global)As we can see, users expect a range of functionality that is not yet implemented by many banks. Therefore, to stay competitive, traditional players must adapt to customer needs at a much faster rate.

What does this mean for banks?

To serve customers faster, banks need to review their processes and identify bottlenecks that could be addressed with innovation and digitalization. For example, as the lengthy manual Know Your Customer (KYC) validations slows down account opening, banks need to find ways to automate the process.

In particular, AI-powered systems can be used to recognize data from customer documents, while blockchain and digital identity solutions can accelerate audits. Robotic process automation (RPA) could enable bank employees to facilitate document-related workflows. E.g., this story describes how a provider of investment management services automated manual extraction of necessary content from financial reports.

While KYC verification mostly affects onboarding, queues and inefficient processes concern existing customers, too. The functionality allowing for scheduling appointments and filling any necessary forms online in advance could greatly reduce the time spent in a branch.

The growing demand for personalization will lead to integrating data analytics tools helping to deliver financial insights based on a user’s income, spending, savings, etc. This is already confirmed by a 2022 survey by The Financial Brand indicating that banks prioritize security, mobile channels, data analytics, and AI for the next 3–5 years.

Still, mobile apps packed with customer-facing features increase the complexity of banking systems and create new potential points of vulnerability. In a March 2023 report, the World Bank listed security as one of the main digital banking challenges, as cyberattacks can compromise business continuity, leading to reputational and economic damages. As such, financial institutions need to invest in operational resilience frameworks, the report suggests.

As more customers want to see innovative features in their apps, banks might run into technical challenges when integrating new software with existing, legacy systems. While mobile banking apps tend to be built with modern frameworks and programming languages, the same cannot be said about the core banking software. Based on technologies created decades ago (e.g., COBOL), many of these systems are difficult and expensive to maintain or integrate with newer applications.

That’s why 69% of banks do not intend to replace legacy core systems as part of their digital transformation, according to the Digital Banking Report issued in June 2022. McKinsey estimates that switching to a new core system could cost large banks around $300–400 million, while medium-sized institutions may still need around $50 million.

For those banks that decide to update core software, a microservices architecture can make future maintenance easier. By breaking down the monolithic core software into smaller components, banks will be able to add new features without having to replace the entire system. McKinsey recommends banks to conduct the transformation in small, incremental iterations, rather than trying to replace the entire system at once.

Finance is one of the most heavily regulated industries, so maintaining compliance can also be challenging when developing mobile apps. Banks need to follow region-specific laws, such as the Electronic Fund Transfer Act (EFT) or the Electronic Signatures in Global and National Commerce Act (ESIGN) in the US. In the EU, digital banking software needs to adhere to the Strong Customer Authentication (SCA).

Consumer needs transform workforce/operations

Banks are accelerating digital transformation, as customers preferences shift to a personalized and seamless experience across mobile channels. The competitive landscape is also shifting rapidly, as traditional players are facing pressure from new entrants, such as FinTech companies and neobanks.

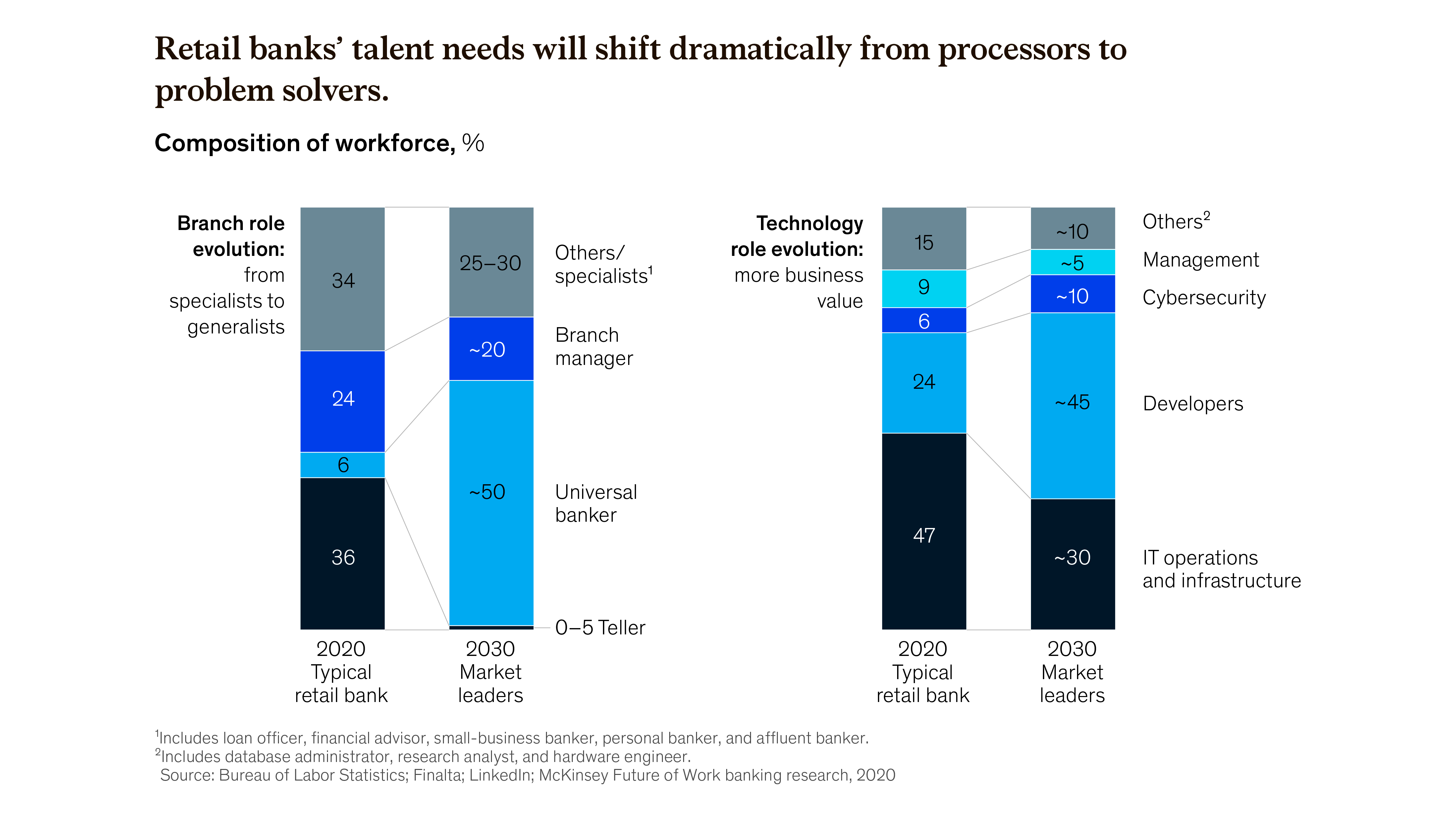

McKinsey recommends banks to work like a technology company, adopting a “digital-first” mindset and streamlining processes to meet customer expectations. This will have significant implications for the banking workforce—e.g., increasing the need for technology-related skills. Organizations will likely need to train employees in data analytics and other intelligent tools to provide insights and act as customers’ financial advisors.

Technology is expected to change the banking workforce (source: McKinsey)

Technology is expected to change the banking workforce (source: McKinsey)At the same time, automation will inevitably have an impact on many routine tasks, such as invoicing, accounting, identity verification, and customer service. As a result, McKinsey estimates that a typical branch staff composition will shift away from tellers (comprising 36% now) to universal bankers (50% by 2030).

To introduce enhanced digital services (like this one), banks will require more developers to build and maintain new products in an agile manner, the report projects. As banks adopt cloud platforms for managing infrastructure and IT operations, McKinsey predicts changes in the composition of the technology workforce, too. By 2030, the share of IT operations and infrastructure engineers is expected to decline from 47% to 20%, while developers go from 30% to 45%.

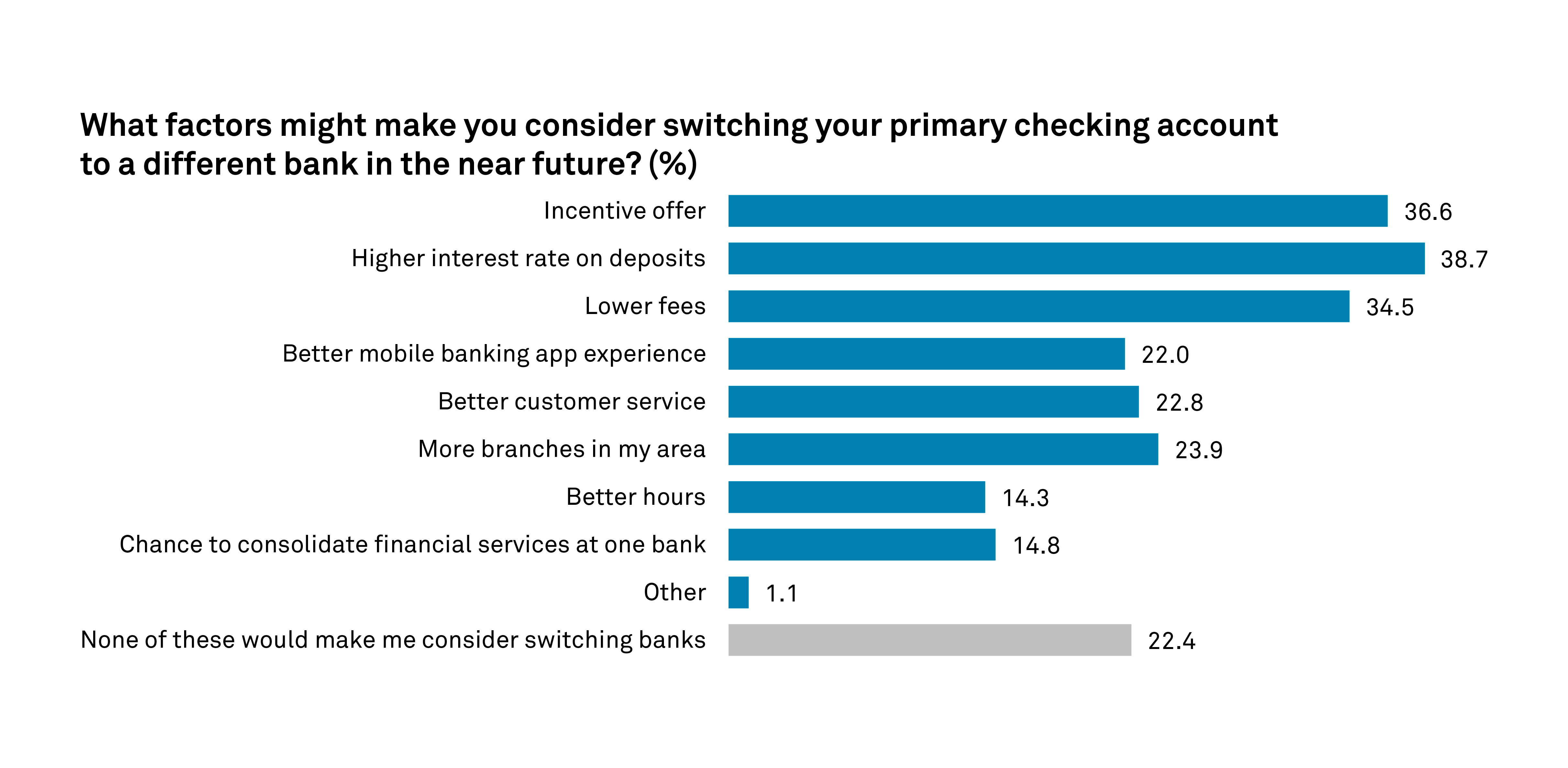

Mobile apps matter when choosing a bank (source: S&P Global)

Mobile apps matter when choosing a bank (source: S&P Global)In this digital transformation, customer expectations around analytics, new innovative services, and availability of mobile tools will play a key role. The importance of the mobile experience for users is confirmed by an S&P Global survey across all regions of the US. 13.4%–24.9% of respondents stated that a better mobile app would make them consider switching banks. So, faster adoption to digital consumer demands, fraud protection, and features driving personalization may help banks to stay competitive.

Further reading

- The Technical Aspects of Integrating Know Your Customer Platforms

- Technical Challenges to Address When Integrating Banking as a Service

Subscribe to new posts

Share

Have a question?

Talk to an expertContact us and get a quote within 24 hours